“The only difference between reality and fiction is that fiction needs to be credible.” – Mark Twain.

Fictions reported as absolute truths make us nuts – or at least I hope that I am not the only one that feels that way. Here are two headlines or “truths” in real estate that occur to me as complete fiction:

- “Housing affordability held steady at its lowest level in a decade.” Housing is NOT more affordable (for much of the country, and especially in markets like Denver).

- “This time is not like 2008,” real estate people like to say, “we are not going to have 2008 all over again”, in terms of a housing and/or financial crisis. They point to the fact that the housing market is too imbalanced – i.e. not nearly enough supply to meet the demand, and that it will take years for itself to correct.

You can probably see already how strongly I feel about these topics – but before I go any further, let’s quickly recap the status of the housing market along the Front Range.

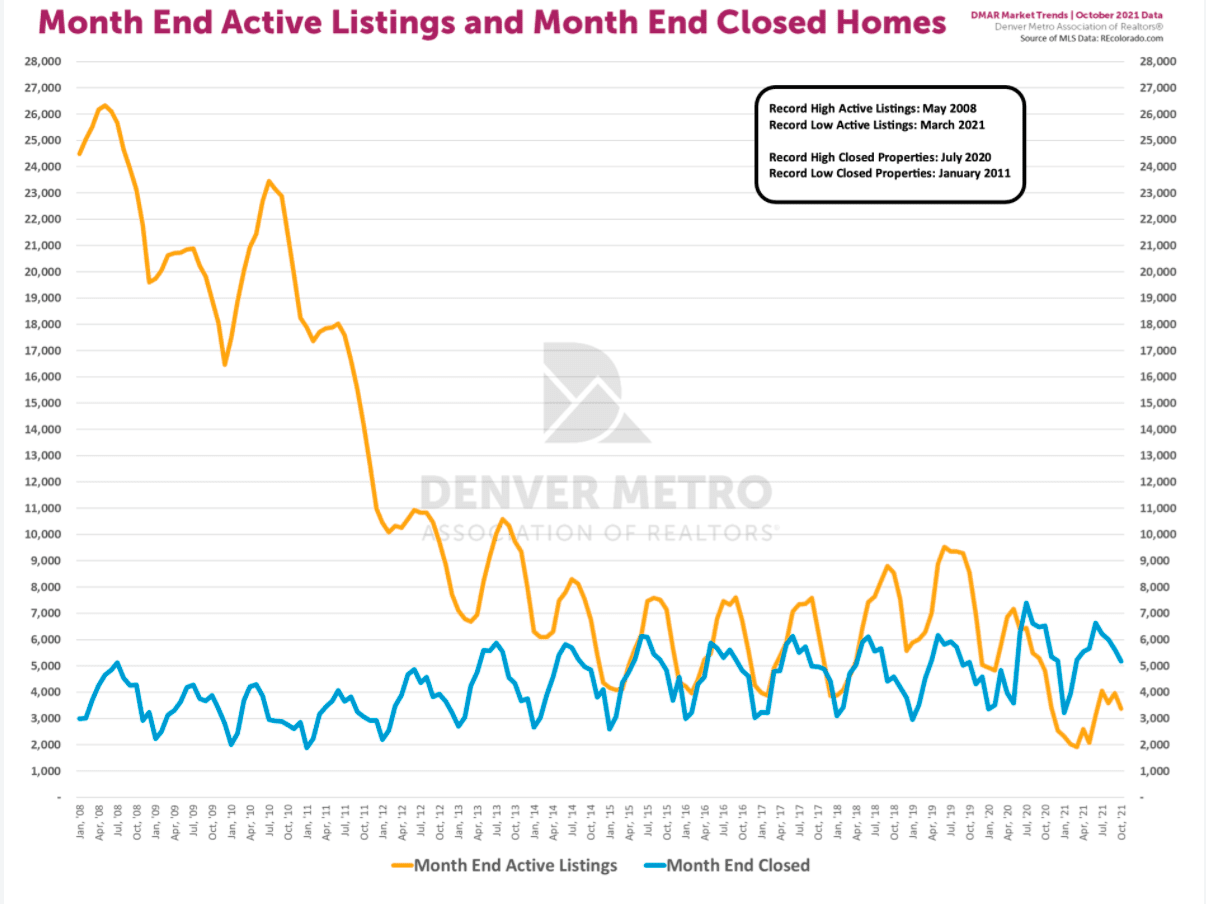

The supply and demand are still completely out of whack: more homes are selling each month than there are actively for sale. Not good for buyers, and prices will not go down as long as this trend continues.

BTW: you can always go to the Denver Metro Association of REALTORS® to get the information I often cite here. Or you can go to the Colorado Association of REALTORS® to get additional data.

Back to the fictions mentioned at the beginning. For all the “Affordable Housing Fairies”, the following example (based in reality) is for you.

In 2010 the median price of a home in Colorado was around $220,000. As of 8/31/21, the median price of a home in the Front Range was $581,000.

Simple math exercise for down payments:

-

20% of $220,000 is $44,000;

-

20% of $581,000 is $116,200.

To “afford” is to be within someone’s financial means. If you didn’t already own a home (and this is a big part of the equation, I understand), where is the extra $72,200 of the down payment coming from?

Ah, well, who cares about down payments? Surely monthly payments are more affordable.

Average 30-year fixed interest rate:

-

August 2010 – 4.43%

-

August 2021 – 2.87%

That’s fantastic! Rates are down! Oh, wait. how does that work for my payment (principal and interest)?

-

In August of 2010, your payment on the $220,000 home would be approximately $854.

-

To buy an August 2021 median-priced home of $581,000, your payment would be $1,927.

Moving on to the second fiction: “this is not a bubble” and “this is not 2008 all over again.” Of course not. Since when do any two crises start the same way? In the 50 years that I have been alive, here are the ones that I can recall (off the top of my head):

-

2008 Housing and Financial Crisis – i.e. The Great Recession

-

2000 dot com bubble

-

Mid 1990’s: SoCal housing downturn through the 90’s as aerospace was decimated, people left California in droves. Prices were down 25% or more; foreclosures were prevalent.

-

What about the downturn during the early 90’s during the first Iraq war?

-

The S&L crisis in the 1980’s (BTW: The ultimate cost to taxpayers was estimated to be as high as $124 billion)

-

The oil crisis and inflation of the 1970’s (and into the 1980’s)

-

(Then there are all the other “local” crises that happen in markets around the country. I mentioned the one in California in the 1990’s; Denver and other markets have had their share too.)

While this is not an apples-to-apples list of events, nor even an exhaustive list, is it totally unreasonable to say that stuff happens (typically) at least every decade that has significant economic effects. AND. that each one of these is relatively different in how they come to bear? We haven’t had another oil crisis. The S&L crisis was not the same as the financial crisis of 2008. Why would the next ‘crisis’ be the same as the last one?

I am not even making a case that housing will crash. The point I am making (and usually make every month) is that “stuff goes bad,” and when it does, like the trash that the kids forgot to take out, it stinks up the whole house. Looking to the last crisis is probably not an accurate prediction of what the next downturn will look like. But there are similar patterns for concern: significant asset increases, people making rash decisions (

in the home buying process), and investor speculation and investment.

While I have no idea what housing will look like for the next decade, here’s a scenario that is actually worse than it sounds: What if housing prices went down only 10% for the next 10 years? Is that so bad?

Maybe not. On the other hand, during that time, what if interest rates were back at 5% (or higher)?

-

The affordability would be even worse than it is now.

-

Who would want to move when they have a rate of 3%? Further, the house they would be moving to would carry an interest rate of 5% – how many people wouldn’t move? Yet, people have to move every year – job changes, family or life changes, etc.

-

Maybe prices don’t fall (although I think they would), but maybe it would likely take a LOT longer to sell a home. No one remembers what it was like to have their home on the market for 9, 12, or 15+ months. .and certainly not all the people who are 35 or younger. Side note: I don’t think most people are prepared (psychologically at least), for any significant downturn in the economy. To my mind that only makes the next downturn (read: economic shock) even more significant.

I think it’s pretty clear that housing is not more affordable, and not getting more affordable any time soon. And as far as economic cycles go, well, I don’t know that I have demonstrated anything other than maybe to consider that whatever is ahead may look different than where we have been (and even that may be a stretch).

For the real estate market, here’s what to look for over the next 6 months.

-

Home prices will almost certainly continue to go up through June 2022 (I am talking specifically about Front Range real estate; although I suspect this to be the case in many other markets across the country). Historically prices almost always go up through the spring, which is the busiest time of the year (NOT the summer!). FYI – home prices did not fall in the spring of 2009, nor spring of 2010. Since there appears to be no immediate end to our current shortage of homes, it seems almost impossible for prices not to go up again this spring.

-

Interest rates seem likely to finally rise. The Federal Reserve has begun to wind down its bond-buying programs. Inflation continues to stay strong. It also seems unlikely that interest rates will stay at 3%. Remember, every 1% of interest rate = 10% of the purchase price when it comes to a home buyer’s monthly payment when they are getting a loan. If mortgage rates go to 4% by next summer, that’s the same as another 10% increase in pricing (as it relates to what a borrower would pay in monthly payment).

So, if you were going to buy in 2022, now would be the time. Of course, this time of year there are fewer homes to choose from, and buyer activity (read: competition) remains strong. If rates begin to creep up next year, look for many calls to buyers of “hurry, act now.” That would only fuel more significant price increases.

These are my musings for the month. For any specific questions on how this relates to your situation, feel free to reach out!

All the best,

Steven