Look, I know I am a broken record. I say the same thing over and over and over...and over.

Lately, as I have made my way through real estate offices I heard this ridiculous question: "When is household income going to increase to catch up the lack of affordability in housing?"

The answer: never. Household income is NEVER going to increase two or threefold in the near future to make housing more affordable!

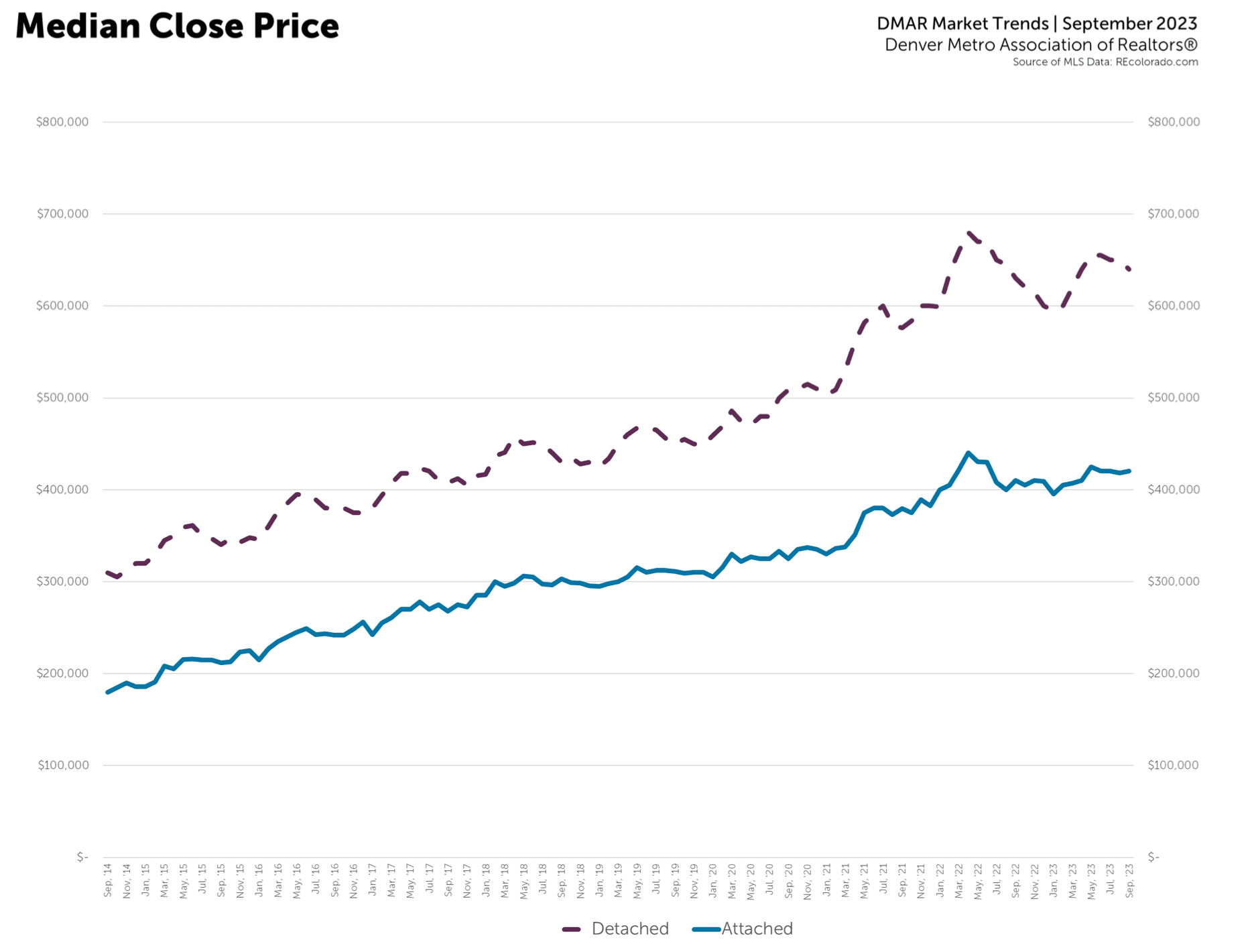

I have said this many times over the last few years: the price of housing has completely run away from average household income. It has always been a looming problem - rather, it has been a looming problem over the last decade. I also said that mortgage rates would eventually go up to a number much greater than where they hung out during COVID (they were mostly in the 3% range). My guess at the time was 6%+ - I had no idea it would get to almost 8% during the past few weeks...but now we're here!

It has become obvious that many people cannot afford to move. They simply are unable to buy homes at current prices with current mortgage rates.

What will solve this problem? Lower prices!

Sellers don't want to hear this. Real estate agents don't want to hear this. The real estate industry as a whole doesn't want to believe this. I am not saying there will be a crash in U.S. housing prices. There could be, but that's not my point.

My point is that there are two variables right now that face would-be home buyers: home prices and financing costs. I think it's safe to say we can take household income off the table as a variable that can easily be affected in the aggregate. If you are a seller who needs to sell before the end of the year, what can you do to move the house? Lower the price.

Yes, I know - those are three dirty little words sellers don't want to hear. Furthermore, both the sellers and many real estate agents don't understand this very simple formula: one percent of mortgage interest is equal to 10% of the purchase price when it comes to monthly payment. Interest rates are up more than 4% over the last two years (3% --> 7%+). If you reduce the price of a home by 40% then the buyer has the same monthly payment as when the mortgage rates were 3%.

Wait - did you just say sellers need to reduce their home prices by 40%???

Kind of.

I mean, I don't think it will take a 40% reduction in list price to move property this fall/winter. On the other hand, in several cases, 5%-10% is simply not going to cut it. By the way, seems egregious to many sellers right now!

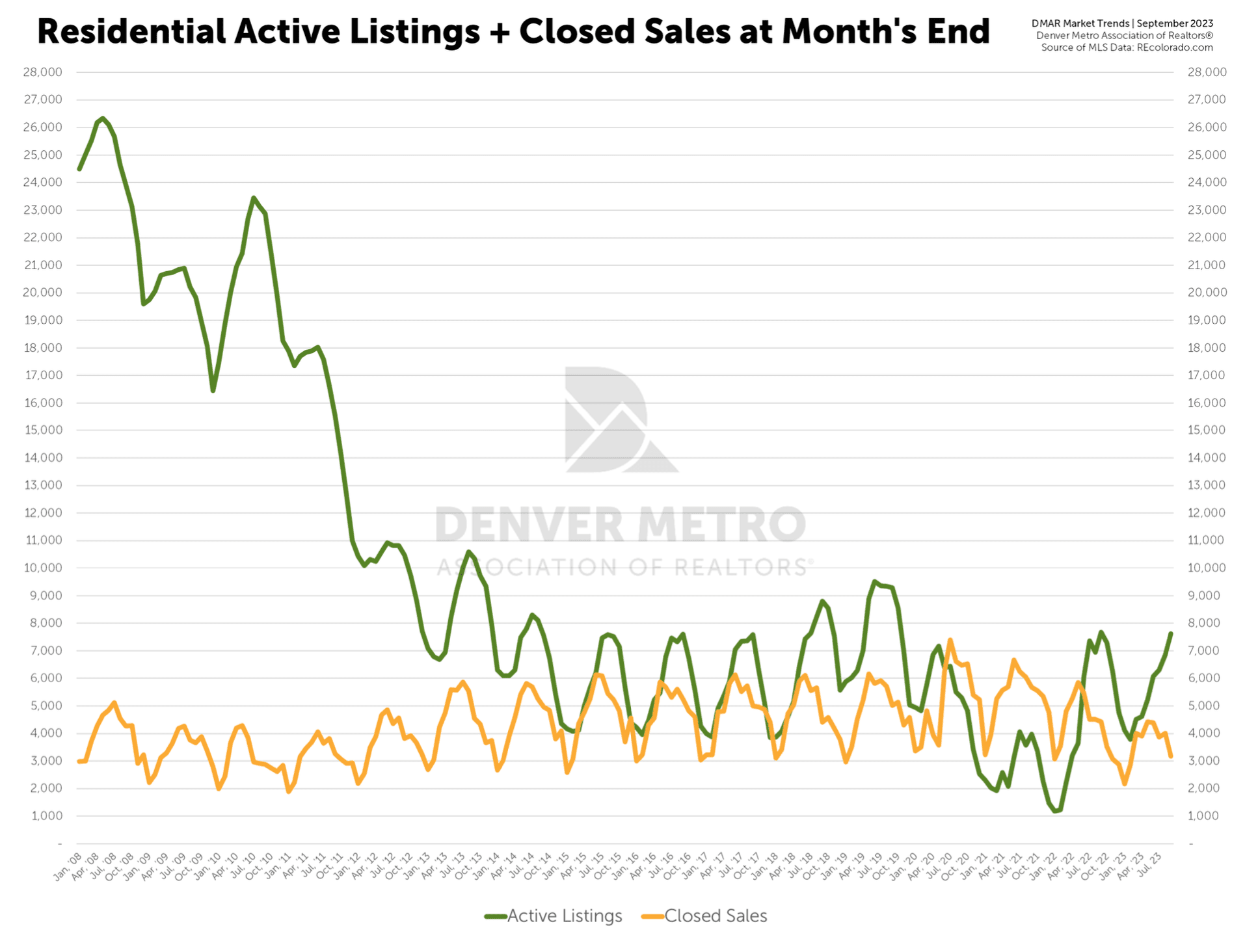

As I write this, it dawns on me that we continue to be in uncharted waters. First, we never saw the historically low inventory and historically low mortgage rates. Then we saw rates move up so far so fast. Now we find ourselves in a situation that is also uniquely ironic. We still have a shortage of homes on the market, but days on market continue to climb, and buyers continue to be frustrated at the lack of choice - and affordability. Many industry folks are clamoring for "lower rates" to "solve this problem."

I don't think this is a problem that "requires solving". The market will gently guide some sellers to give back the over-generous gains they were given from the real estate gods over the last few years. If you are upset by this statement, please keep in mind a) this doesn't apply to you if you aren't moving, and b) Nowhere in the history of the last 100 years is it reasonable for home prices to go up 40% or more in less than a three year period (on top of the 100% increases coming out of the 2007-2009 recession).

Note: I am mostly speaking about the local Denver Metro market. However, there are many other parts of the country that seem to be experiencing the same phenomena.

|

|