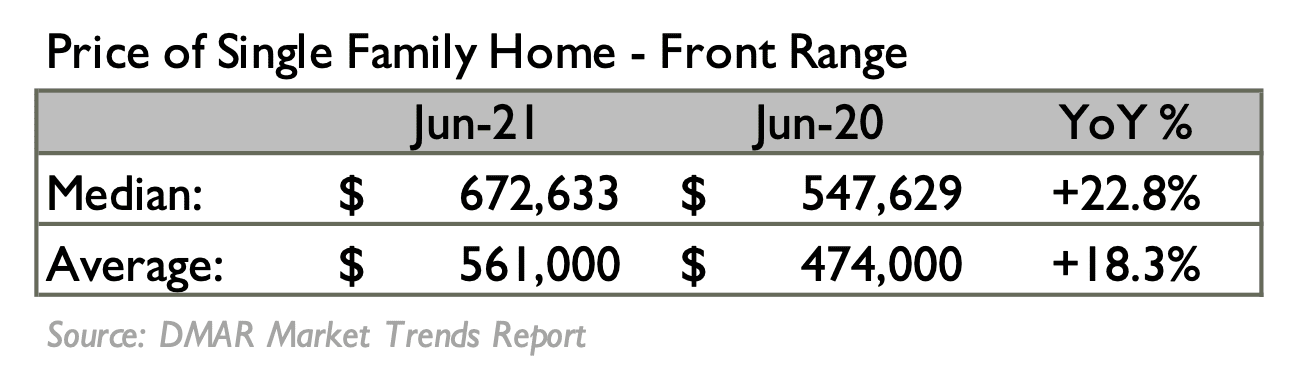

We are marching through summer with real estate prices in line with the weather, and there seems to be no change in the dynamics of the real estate market. Continued out-of-balance supply and demand have led to substantial year-over-year price increases.

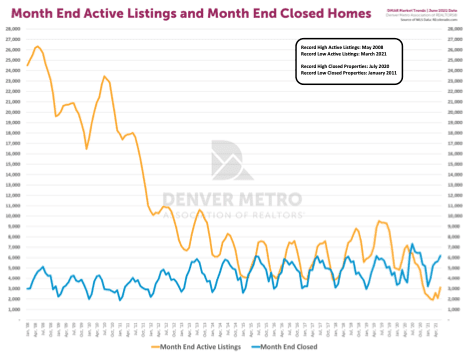

The only thing that appears almost normal is that we seem to be following the usual market seasonality: highly active spring followed by a summer slowdown. Typically, when we get to the July 4th holiday, housing inventory is peaking as showing and sales slow for the summer. Total showings have been softening since May. However, supply is nowhere near the levels it would need to be to have the market balanced. There are simply not enough homes that can come on the market to outpace the number of buyers who would still like to purchase. Therefore, prices are not likely to soften through the summer/early fall as they typically do, on the other hand, prices do not seem likely to continue at the same frenzied pace seen through the spring.

The Bigger Picture

As usual, I like to pontificate on what might happen next, even though I have absolutely no clue. Here’s what’s on my mind:

- Interest rates – I think everyone can clearly see the compelling price increases in the economy (cars, gas, housing, food/restaurants, etc). How can inflation be well above 3%, yet 10 Year U.S. Treasury and hence mortgage rates have been pushed lower over the last 30 days. This leads me to.

- The Federal Reserve – I have said before that the Fed’s continued purchase of Treasury bonds and mortgage-backed securities seems like a bad idea, and now someone with a lot more experience and credibility than me has publicly said the same thing. Bloomberg recently reported, “Former Treasury Secretary Lawrence Summers said the surge in U.S. house prices is “scary” and questioned the wisdom of the Federal Reserve continuing to purchase mortgage-backed securities as part of its stimulus campaign.” Summers also said that “Rising house prices in most people’s common sense of the world represents inflation.” Having said that, I also know if I were the Federal Reserve Chairman, I have an impossible task. No matter what I do, I am not going to get it quite right, and there are always unintended consequences to every action I take.

- Other Pricing/Inflation: Gasoline – Andrew Ross Sorkin reported in his DealBook newsletter that since World War II, we have had 6 periods where inflation was greater than 5%. The last three were all related to oil. While oil has many uses, you and I mostly relate to oil as to what we pay at the pump. Unleaded gas where I live has gone from approximately $2.26/gallon on January 7th to $3.49/gallon on July 14th. The AAA is reporting that gas could increase an additional 20 cents. Of course, if your car requires premium unleaded, add another 70-80 cents.

- Housing Supply – I seem to have missed connecting ALL three of the following dots: formation of new U.S. households, under-building of single-family homes, and the Great Reshuffle (people leaving urban attached dwellings for suburban homes). Per the latest census data, the U.S. formed 10.9 million new households from 2010-2020, yet only produced 6.5 million new single-family units. Did the “Great Reshuffle” move that many people from urban multi-family (apartments, condos) into suburban homes? Is that why we have no homes for sale – anywhere in the country?

- Housing permits and starts are up across the country, per the National Association of Home Builders. Here in Colorado, there is new development happening, it’s just outside of Denver. A couple of examples: between Lone Tree and Colorado Springs there are plans in various stages for thousands of new homes; Sterling Ranch (between Highlands Ranch and Sedalia) is on its way to adding 12,000 total units when the project is completed.

What does all this have to do with people like you when it comes to making decisions about real estate? Real estate markets work in cycles, and this has been one very long, very large appreciation cycle. Does anyone remember all the empty, foreclosed homes of the Great Recession? Is it impossible to think 10 years from now we could be right back to where we were? This also reminds me that not too many years ago there were a lot of people who lost money in real estate. It can and does happen.

If you are faced with some decision regarding your real estate, whatever decision you make – to buy or to sell, or not to buy or not to sell – could you be okay with that decision for the next 7 to 10 years? Why that long? People who bought at the height of the last cycle – it took a long time to make up for lost ground, but it did make it up eventually and then some. (By the way: past history doesn’t guarantee future results.)

If you have no plans of buying or selling, then it probably makes no difference what the market does along the way.

Bottom line: over the next 6 months I am expecting to see no relief of housing inventory (continued shortage of homes for sale, although maybe not as extreme as it has been during the first 6 months of this year). Prices are not likely to fall if the housing inventory stays the same and especially if mortgage interest rates stay between 3%-3.5%. If however, mortgage interest rates did resume their climb back up, and they got to 4% or more, I would expect to see more inventory and some easing of pricing, albeit small.

As always, I am here to help.

All the best,

Steven